Financial institutions around the country are anticipating the release of additional HMDA data in early May. New data is coming; it will be different and have more depth. This blog will cover what will be included, what you need to know, and how to prepare for the May 2019 HMDA data release.

The last few years have been chock-full of regulatory changes to the Home Mortgage Disclosure Act (HMDA). Everything from data collection to the public HMDA LAR release has undergone updates, and the challenges continue to mount.

Compliance professionals nationwide are in the midst of another seismic shift in the HMDA compliance landscape: the release of the expanded HMDA LAR, which is sometimes called the HMDA Plus data.

Today, you’ll learn all about the ongoing release of the public 2018 HMDA LAR data. We’ll dive into the most important changes, some potential challenges, and how to prepare for the upcoming May 2019 HMDA data release.

As mentioned above, some of the biggest changes to HMDA are related to the release of the public HMDA LAR. In particular:

- The data is now released much more quickly, shortening the HMDA lifecycle.

- For many years, financial institutions submitted their HMDA LAR to the regulatory agencies in March, and the agencies released the public HMDA LAR in September. Now, the data is submitted in March, and published within weeks, in keeping with the new HMDA statute.

- These public HMDA releases now include a much broader and more detailed data set, since they include the HMDA Plus data.

- More industry experts, journalists, politicians, and community groups are expressing an appetite for an interest in analyzing this data, and sharing their conclusions with the regulators and the public.

What was Included in the April 2019 HMDA Data Release?

On March 29, 2019, the CFPB released bank-level HMDA data, called the Modified Loan/Applicant Register. The data released is the HMDA LARs for individual institutions; the release included approximately 5,400 financial institutions’ data. These individual institutions’ HMDA LARs for 2018 can be found here. Please note: sometimes this data is referred to as the “respondent-level LARs.”

This HMDA publication marked the first time that any of the additional data points and fields required by the 2015 Final HMDA Rule were released publicly.

What Is the Difference Between A HMDA Data Point and a HMDA Data Field?

“According to the HMDA Rule, a "data point" is basically a small collection of related “data fields.”

For example, there is a "property address" data point. In that data point are a four different "data fields": street address, city, state and ZIP code. That's just one example. There are a lot of different data points with multiple data fields.

Insured depository institutions and credit unions that qualify for the partial exemption may still choose to report those exempt data points, if they want.

That said, know that if you choose on a data point, you have to report ALL of the fields therein.”

- Ncontracts' “Guide to the HMDA Changes”

The HMDA LARs included in last month’s release contains loan-level information on individual HMDA filers, although that data has been modified to protect privacy.

The modifications to the HMDA data include:

- The treatment of some data elements.

- The exclusion of some others, including some of the freeform data.

- Adjustments to make some data elements less precise.

This blog about the recent HMDA data disclosure changes goes into almost-comprehensive detail on this subject. If you’re interested in learning more about what data will be made public, and how, definitely do bookmark that blog.

What Is A Compliance Management System And Why Your FI Needs One

Per the 2015 Final HMDA Rule, financial institutions no longer bear the burden of making their HMDA data available to the public upon request. That is now the regulators’ responsibility. Again, all modified HMDA LARs for individual institutions are currently available to the public on ffiec.cfpb.gov and the 2018 modified HMDA LARs are available here.

For our Fair Lending analysis, Ncontracts utilizes the Dynamic National Loan Level data set that will be released in May, not the Modified Loan/Applicant Register that was released in late March.

There has been some confusion over the past few weeks because the CFPB released these respondent-level LARs, but many Fair Lending software solutions (including Ntransmittal) need the national-level data set for their analysis. That is, in a nutshell, what we’re waiting for in early May.

Let’s learn a little more about the HMDA data that will be released in early May 2019.

What Will Be Included in the May 2019 HMDA LAR Release?

As mentioned above, the CFPB has made it clear that they will release additional HMDA data beyond the modified HMDA LARs. The May 2019 publication of the HMDA Dynamic National Loan Level data is expected to include:

- A complete loan-level dataset.

- The aggregate HMDA LAR.

- HMDA disclosure reports.

- Certain new data points, which are likely to reveal even more about mortgage lending in the US.

According to the CFPB, this release will also include a Data Point article that highlights key trends.

Don’t forget that both exempt and non-exempt lenders are included in the HMDA data release. Even if your financial institution isn’t required to collect and report all of the new data points and fields, your other HMDA data will be released.

We are anticipating that this May release will spark much more HMDA analysis, and we’re not alone in that. The Bureau has also noted that they will be “applying particular rigor and analysis to address data anomalies, including in the new data points and describing the context in which the data may be best understood.”

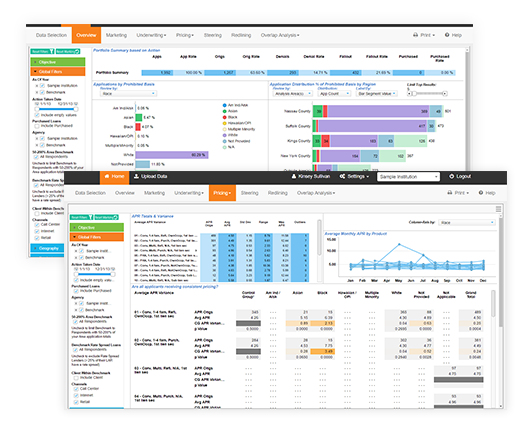

The right HMDA software will make analysis, reporting, and submission clear and insightful. If you’re looking to improve your HMDA compliance, know that Ncontracts can help.

How Will this Public HMDA Data Be Used?

The public availability of this data is almost certain to spark controversy, as it contains more information on applicant and borrower demographics, products, loan features, underwriting, decisioning, and the competitive landscape than ever before.

Consumer watchdog groups, journalists, and politicians were eager to get their hands on this data. For some, it may support an existing or previously reported perspective on race-, ethnicity-, or gender-based housing discrimination in the US. For others, it may help prove that great progress has been made. For financial institutions caught in the cross-currents of these powerful narratives, this public attention can present a real challenge.

Regulatory agencies also use this data to prioritize financial institutions for Fair Lending examinations, based on potential disparities and risks that may be present in the HMDA data. Data analysis is a critical part of Fair Lending risk management, and is often part of Fair Lending risk assessments. Remember, disparities do not always mean discrimination, but analyzing your data is the only way to know for sure!

Ncontracts Viewpoint: It may be tempting for some to look at this data and try to “prove” housing discrimination. That would be a mistake. For one thing, a reviewer needs to know what the data says and how it should layer and relate to each other. For another, there are many qualitative factors, like compliance culture and policies and procedures, that must be considered.

The exciting part of this public HMDA data release for you, the financial institution professionals, is that this data opens up new ways to analyze HMDA data, reduce your Fair Lending risk, and tell your story.

With the availability of this expanded HMDA Plus data, HMDA analysis becomes much more important for financial institutions. Know that we are here to help you with your HMDA compliance goals!