2019 has been a big year for Fair Lending news. In this post, we catch you up on the latest.

Fair Lending has been in the news a lot in 2019, and there have been several lessons learned. From HMDA data to Redlining risk and small business lending, there was plenty of knowledge to gain from the first three quarters of the year. Now that we're at the end of October, what's the latest?

- HMDA Final Rule Extends Small-Filer Threshold Two Years

- Bankers Say Fair Lending is a Fairly Risky Business

- CRA Compliance Pressure Leads to More Business Lending and Higher Defaults at Smaller Banks

HMDA Final Rule Extends Small-Filer Threshold Two Years

Earlier this month the Consumer Financial Protection Bureau issued a final rule that extends the current Home Mortgage Disclosure Act (HMDA) temporary small-filer threshold for collecting and reporting data about open-end lines of credit for two more years, until January 1, 2022.

Financial institutions that originated fewer than 500 open-end lines of credit in either of the two preceding calendar years will not need to collect and report data with respect to open-end lines of credit in reporting years 2021 and 2022.

While the extension didn’t come as a surprise, it was unusual that the CFPB issued the rule just days before the comment period was expected to end—essentially eliminating the last four days of the small-filer comment period. The bureau had reopened the comment period on July 31.

In 2022, the threshold will revert back to 200, although the CFPB says it plans to issue a separate final rule in 2020 addressing these thresholds.

Bankers Say Fair Lending is a Fairly Risky Business

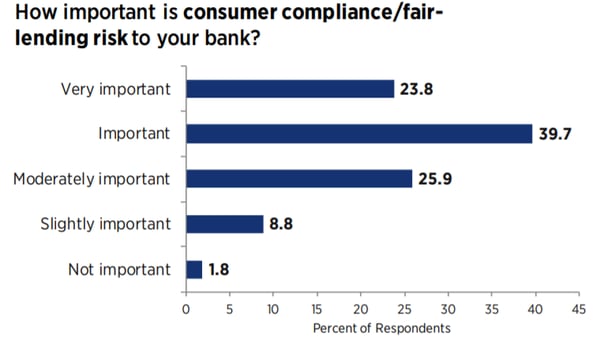

How important is fair lending/consumer compliance risk across the community banking industry? Nearly two-thirds of community bankers say “important” (39.7 percent) or “very important” (23.8 percent), according to the 2019 Conference of State Bank of Supervisors National Survey of Community Banks as part of the Community Banking in the 21st Century Research and Policy Conference.

Source: CSBS

It’s about the same amount of concern management succession risk, BSA risk and operational risk receive. Areas like legal risk (one-third saying it's important or very important) and board succession risk are lower on the totem pole.

Top of mind is cybersecurity, which topped the list as the most important risk (70.5 percent say it’s very important), followed by credit risk (44.9 percent say it's very important).

CRA Compliance Pressure Leads to More Business Lending and Higher Defaults at Smaller Banks

During Community Reinvestment Act examination years, small banks make more of their smallest business loans, but shift the risk of higher defaults onto the government by funding them with Small Business Administration guarantees, according to a study.

At the 2019 Community Banking in the 21st Century Research and Policy Conference, the conference committee announced the paper that made the “most significant contribution to banking policy” in 2019. The paper, “Who’s Holding the Bag? Regulatory Compliance Pressure and Bank Risk-Shifting,” by Lamont Black at DePaul University and John Hackney at University of South Carolina, finds CRA compliance pressures lead small banks to a 19 percent boost in smallest business loan origination at small banks. There is no corresponding increase at large banks. These loans have a higher rate of default, are less likely to be revolving loans, and are more likely to be funded with SBA guarantees.

“The paper concludes that more CRA-induced lending leads to a short-term increase in employment for local small businesses but it also results in a long-term decrease in employment as the increased risk of the loans made in CRA exam years is realized,” the conference notes.