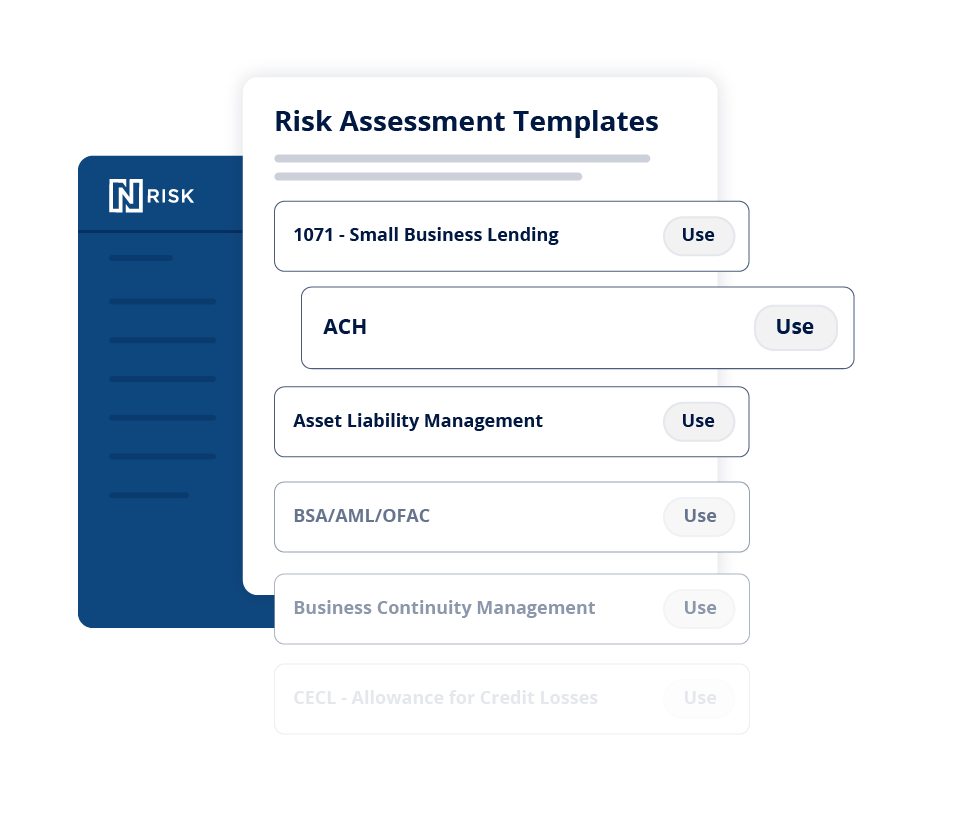

Get a real-time, bank-wide view of risk

Ready to ditch fragmented reports and manual processes? Move beyond siloed risk management with scalable cloud-based enterprise risk management software for banks. Gain a holistic view of risk with real-time insights and expert-built controls. Collaborate across departments with customizable risk assessments, ratings, and reports. Proactively manage and mitigate risk to keep your bank aligned, agile, and ready for what’s next.

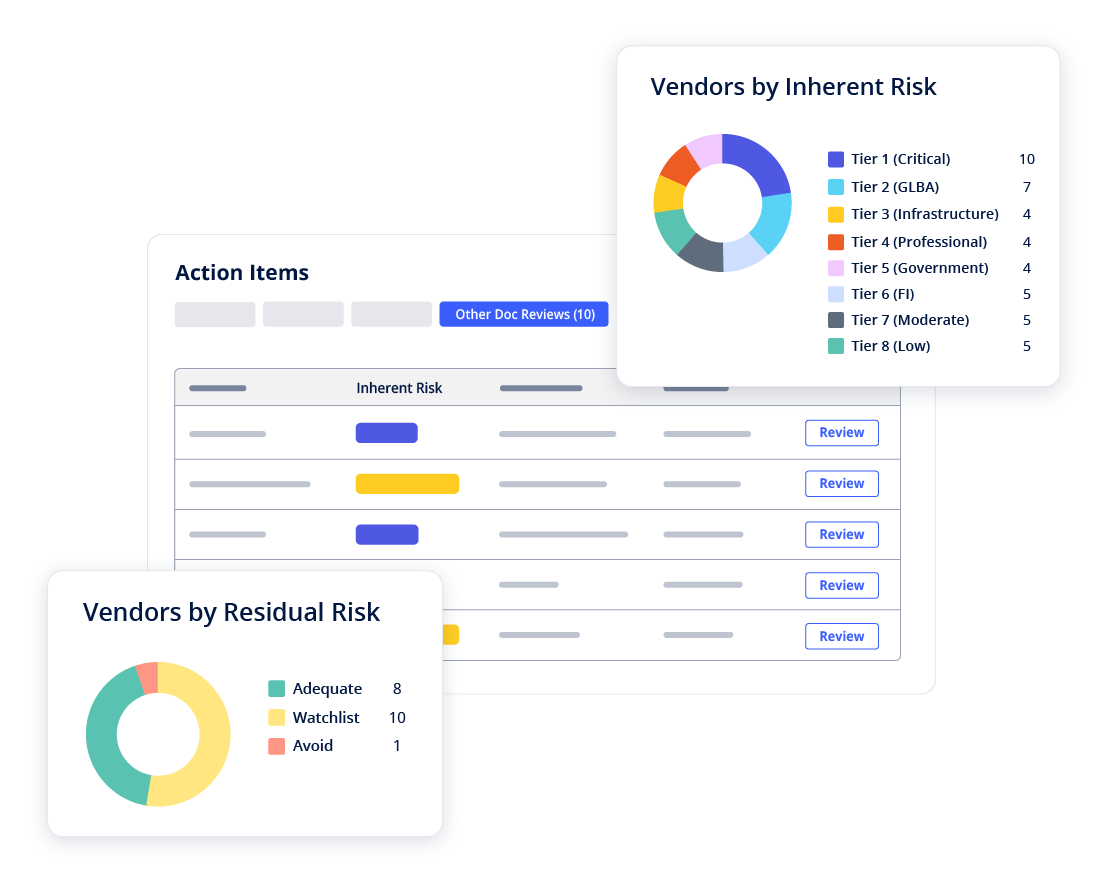

Manage third-party risk with confidence

Does your TPRM team need support? Centralize vendor data, automate due diligence processes, create customized vendor risk assessments, and manage contracts in one comprehensive third-party risk management solution. Easily track compliance, operational, cyber, and financial risks — and reduce internal workload with vendor services that analyze due diligence documents and support risk reviews — across all your bank’s third-party providers.

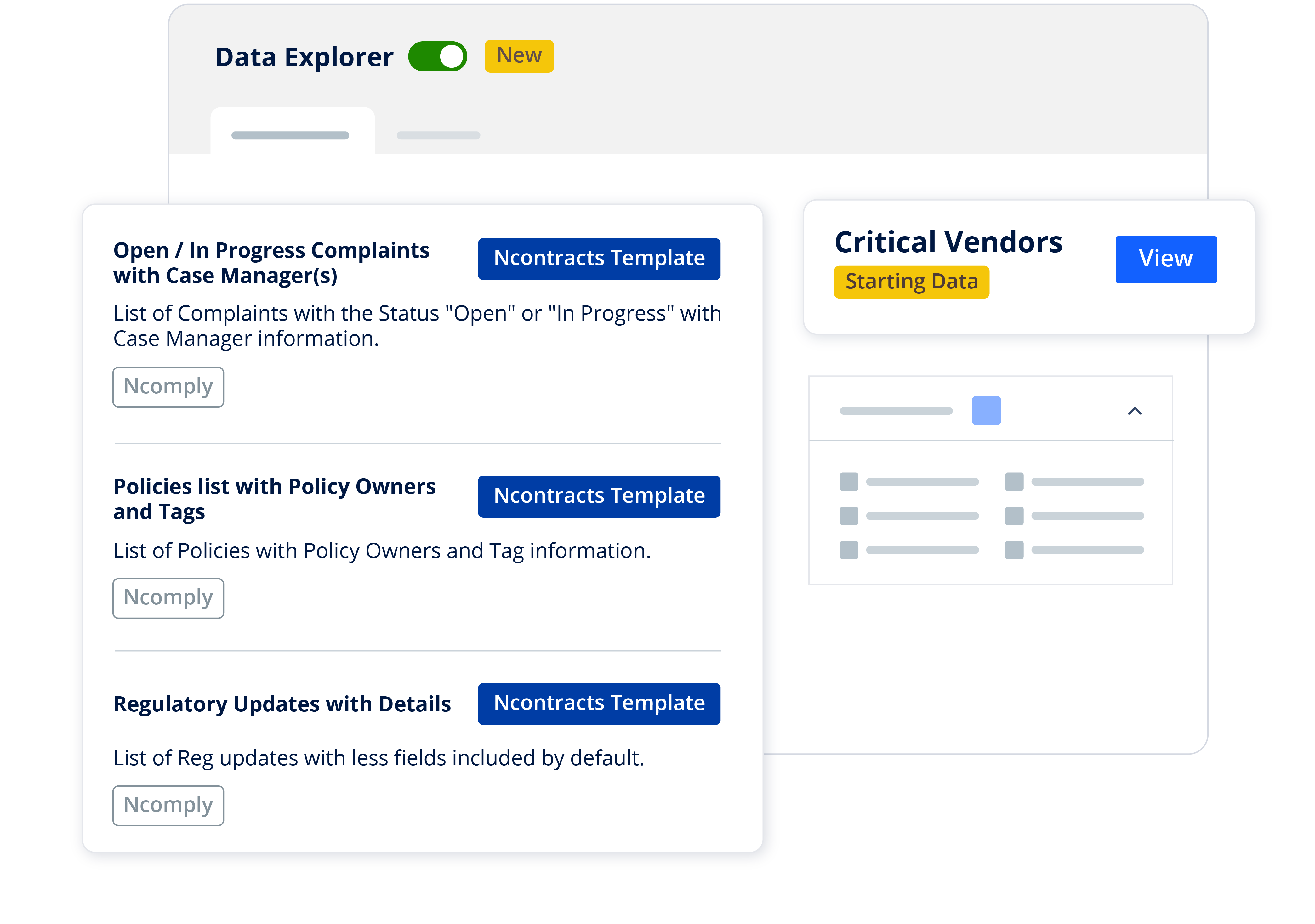

Simplify regulatory compliance

Struggling to keep up with complex and ever-evolving banking requirements? Stay exam-ready with a banking compliance software that takes the guesswork out of compliance. Empower your team to stay proactive with automated tools that manage policies, track complaints, and create examiner-ready reports — all in one platform. Access plain English explanations of state and federal banking regulations. Daily library updates aligned with your bank’s profile ensure you never miss relevant changes. Save time and reduce risk throughout your bank.

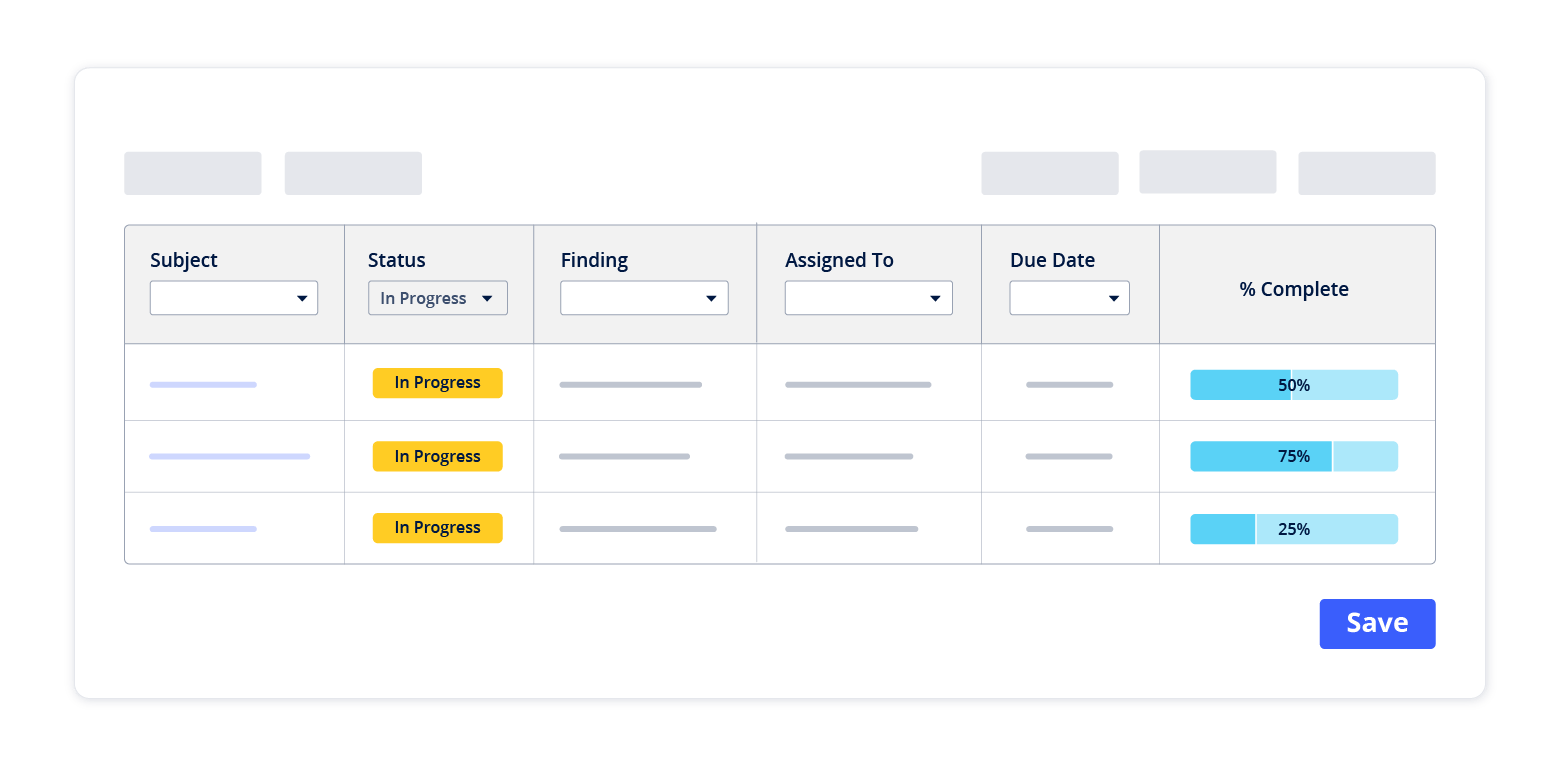

Track and address findings — fast

Ready to transform how you manage audit, exam and other findings? Confidently track, resolve, and document issues from internal audits, compliance reviews, and regulatory exams — all in one centralized platform. Gain real-time visibility into findings, automate task reminders, prioritize remediation, and maintain a complete audit trail. Go from issue to exam-ready reporting with tools that ensure nothing slips through the cracks.

Improve productivity with advanced auditing

Is your bank maximizing your internal audit processes? Reduce your team’s manual efforts by consolidating audit planning, execution, and reporting in a single system. Customize audit templates, automate workflows, and integrate exam and audit findings management for holistic risk tracking and remediation. Discover operational redundancies and areas for improvement for a smoother, faster auditing process.

.png)

The CRA Examination Process Explained: What Banks Need to Know

CFPB Finalizes Small Business Lending Rule (Section 1071)

.jpg)

Laws vs. Regulations vs. Rules vs. Guidance: What Are the Differences?