Many organizations think of culture as a north star that guides internal decision-making, but it’s also a useful lens for viewing partnerships, as we were reminded at the 2022 ABA Regulatory Conference in Orlando, Fla.

The topic came up during the session Building a Compliance Risk Management Framework for FinTech Partnerships. The speakers highlighted the different risk cultures of banks and fintechs and how bridging those differences is essential to working together effectively.

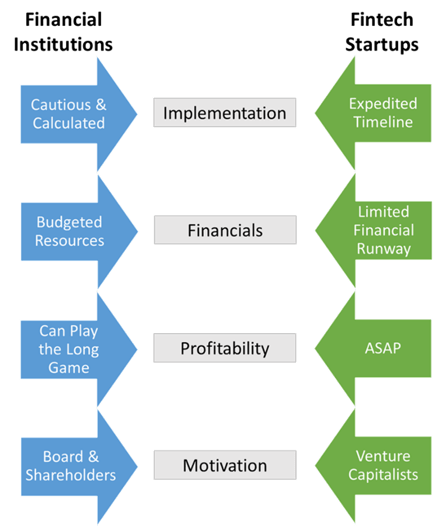

It’s something we talk about with our bank, credit union, mortgage company, and fintech customers regularly. Just consider the cultural differences between financial institutions and fintech startups.

Startups and regulated financial institutions are bound to have major cultural differences, especially when it comes to compliance risk and third-party risk. One organization has a limited runway and needs to achieve profitability quickly. The other has more stable resources but is accustomed to moving more slowly and deliberately to ensure it is in lockstep with regulatory expectations to avoid the pain of regulatory enforcement actions and fines.

Related: Culture and Conduct for Financial Institutions: Ncontracts and Risk Management Association (RMA) Discuss Survey Results

This can lead to conflict if not addressed early on. Fintech startups must understand that highly regulated financial institution have exacting standards because they need to comply with strict regulations. Financial institutions must recognize that fintech startups need to balance the needs of the financial institution with the fintech’s own growth needs.

Aligning expectations for effective partnerships between financial institutions and fintech startups

Building an effective partnership between a financial institution and a fintech startup requires clear communication from the very beginning.

Sharing key terms, goals, and metrics for success can help put everyone on the same page.

For example, if a partnership’s key goal is to maximize efficiency, both parties must agree what efficiency means and how it’s measured. (These are the types of elements that make contract management such a huge part of initial due diligence and ongoing monitoring.) It could mean doing the same amount of work with fewer employees or more work with the same number of employees. It could mean improved communication and collaboration, spending less, or an easier way to employ remote employees. It can mean reducing the number of meetings or eliminating unneeded products or processes.

The conversations can help develop key performance indicators (KPIs), a valuable tool for measuring and monitoring risk.

It’s a concept the session speakers touched on when discussing the value of creating and following a fintech playbook. Every institution should have a playbook that governs all aspects of fintech partnership relationships, including vendor management, risk, compliance, business continuity, etc.

They also kept repeating how absolutely essential initial due diligence and ongoing monitoring are.

Setting the stage with a compliance risk framework

Culture is just one element of a compliance risk framework. And while it may not seem like a top priority compared to due diligence, policies and procedures, regulatory change management, and ongoing monitoring, I’d argue culture is an essential building block for the entire compliance risk framework. It forces an institution to look at itself as well as its potential partner. It informs decisions about risk.

Related: Compliance Risk - Avoid Vendor Compliance Failures by Properly Assessing Risk

Good fintech partnerships don’t happen by chance. They require a strong risk and compliance management framework that helps everyone involved minimize risk and maximize opportunities for growth and success.

Want to learn more about how to strategically evaluate potential fintech partners, manage fintech partnership risk and avoid the common mistakes that can spell disaster for a relationship?